Promoted by Banjo Loans.

Recent research revealed that only one in five SME's regularly review their funding arrangements and actively shop around for better products and services. Why is this? Perhaps they are already well looked after by their bank? Or maybe they are just disillusioned with the whole process and doubt that they can find truly better deals? We believe that, for many, they simply do not have the time or the necessary insight to find the right funding. This is why we have prepared this smart checklist for those seeking finance for their small business– to be ‘finance fit’.

Preparing your application

Before you apply for a business loan, there are things you can do to improve your chance of success.

Start by considering these factors before you approach a lender:

- How much do you need to borrow?

- What do you need the loan for?

- How long will you need the loan for? Or will you need ongoing funding?

- Do you want to offer an asset as security?

It is also recommended to get professional advice from a qualified accountant or a finance/commercial broker.

Supporting your loan application

Lenders will need to see documentation to support your application for business funding. Take a look at the list below and make sure your application is properly supported:

- Business account books

- Six months of bank statements. You may be able to permit the lender to connect with your bank and acquire this information digitally

- Know your Credit history. You can check your credit history by visiting Get Credit Score

- Proof of up to date ATO or BAS payments

- Profit & loss and balance sheets from at least the previous year, or from the previous two years if possible

- Cash flow forecast statement, including all of your current and upcoming financial commitments

- Proof of Personal Property Securities Register for any assets you want to put up as security. This proves that the assets are not already subject to interest from a financial institution. Check PPSR status by visiting com.au

Choosing the appropriate business loan

When it comes to streamlining your cash flow. There are two major types of business funding to choose from:

1. Line of Credit

A line of credit facility allows you to draw on credit up to a pre-approved limit at any time. This type of loan can be beneficial if your operating expenses are increasing, and you need to access funds on a semi-regular basis to help with your cash flow. There is a maximum limit to what a bank or an alternative finance lender will lend you for Line of Credit. Average credit limit ranges between $10,000 to $500,000 depending on the size of the company.

Common examples of when you may require line of credit funding include:

- Hiring additional staff to deliver new or existing work

- Purchasing inventory

- Paying ATO & Bas

- Developing and launching marketing campaigns and growth initiatives

2. Term Loans

This type of funding provides you with a loan upfront, and is generally for a term of 12 months or more. You are then required to pay back the loan amount at regular intervals, covering both the principle and the interest. The length of the loan term determines the repayment. Common situations in which term loan funding is suitable include:

- Renovating or moving into a new premise

- Purchasing new equipment

- Debt consolidation

- Acquire new businesses

- Fund a management/shareholder buyout

Deciding on a loan term

Generally, deciding on a loan term is relatively straightforward. The shorter the loan term, the less you will pay in interest, so aim to make your loan term as short as your capability to make the repayments allows. Often, term loans are used to fund some kind of business asset, and the term of the loan will typically match the life of this asset.

Of course business cashflow is important here, as this is what will be used to make the regular payments. The cashflow available for debt servicing (CFADS) is the available cashflow after deductions of working capital, financing costs and taxes. This will be used to determine the amount the business is able to repay monthly.

The final decision should be taken based on what suits the business' cash flow conversion lifecycle. For example, if a business takes out a loan for 24 months with a cash flow conversion lifecycle of 60 days, this can create an additional burden as the business will need to constantly boost cash flow to keep up with repayments. It is vital to take your own business' conversion lifecycle into account before deciding on a loan term.

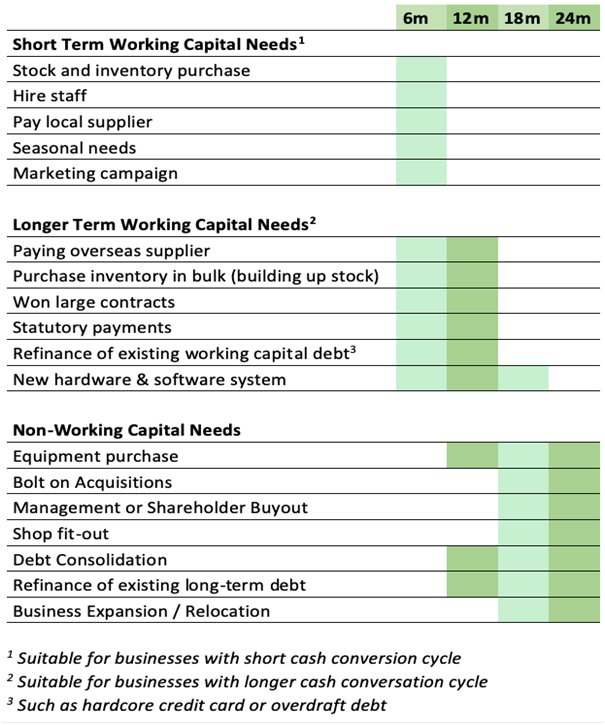

Banjo has come up with a table to demonstrate the needs of the business, and the preferred term for each loan. Take a look below;

Seek professional advice before submitting your application

The above checklist is designed to give you a convenient guide to draw upon as you prepare your application. However, this guide is no substitute for reliable, professional advice.

It is strongly advised that you seek advice from your accountant or finance broker before approaching a lender, to make your position stronger and to give you the best chance of achieving what you need.

Achieving funding for your business can be a tricky process, but it is certainly not an impossible one. By preparing yourself and your business before you begin, you can give yourself a fighting chance at success. What's more, by understanding the requirements of lenders and other financial institutions, you eliminate the frustration, anxiety, disappointment, and difficulty often associated with this necessary business process.