The major bank has hit a “major milestone” of seeing half of new mortgage flows coming from its proprietary channel, according to its CEO.

National Australia Bank (NAB) has revealed that, for the first time in recent history, half of the bank’s new mortgage lending has come from its proprietary channels.

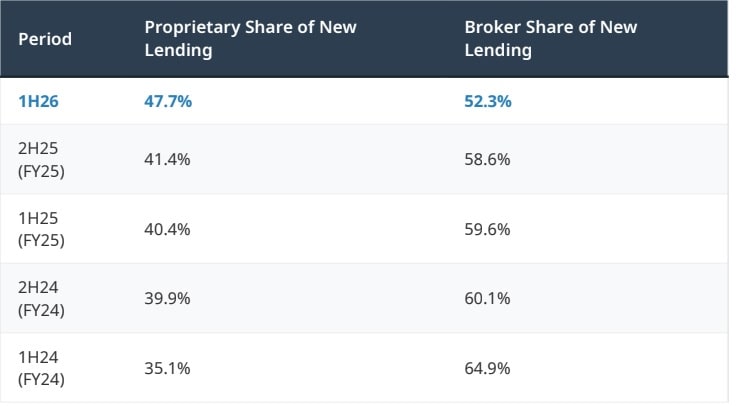

Speaking to media on Monday (4 May), following the bank’s half-year results for the six months ending March 2026 (1H26), the group CEO Andrew Irvine said that while proprietary flows had increased to 47.7 per cent in the half (up from 40.4 per cent in March 25 and 41.4 per cent six months ago), this grew to 50 per cent in March “a major milestone for [the] bank”.

Broker flows fell to 52.3 per cent in 1H26, markedly down on the 59.6 per cent in March 2025.

Brokers are now responsible for 53.8 per cent of NAB’s Australian mortgage portfolio – down from 53.8 per cent in September 2025 and the first time it has dropped in recent years.

The milestone comes as the bank continues to prioritise proprietary lending to increase net interest margin and returns on investment (as first announced in 2024), one of its three core priorities (alongside growing business banking and deposits).

Proprietary lending is actually up 72 per cent across both personal banking and business/private banking since 1H24, according to the major bank CEO.

Irvine said that NAB continues to “navigate the Australian home lending market in a deliberate and disciplined way”, with the increase in proprietary lending supported by improvements in banker capabilities and tools over several periods.

Over the half, it boosted the contribution from its 270 new bankers, as part of its move to continue to grow proprietary lending with “high quality bankers supported by a leading ecosystem”.

The bank said it was also providing “pro-active leads” to bankers via its “customer brain” (which pulls on real-time data to connect bankers to customers “at the right time, with the right action”), enabling them to provide “more targeted conversations improving home loan application outcomes”.

NAB moving to a ‘targeted’ broker strategy

The major bank said it would continue to work closely with the broker channel, but was moving to a “targeted” approach by “deepening relationships with valued brokers to drive growth in priority segments”.

While details of this new broker strategy have not yet been disclosed, when asked by The Adviser why NAB was moving to a “targeted” broker strategy, the NAB CEO explained: “What we want to do is to focus on a smaller cohort of brokers that we have good relationships with, that we can, essentially, more effectively service.”

“We’ll be focusing on those brokers where we believe that we’ll get flows that are closer to our appetite in terms of above cost-of-capital lending. We really don’t want to be doing business where the returns are below our cost of capital. So that’s where we’re pulling away from, slowly and purposefully,” he told The Adviser.

The NAB group CEO said the bank wanted to be “the partner of choice for target brokers”.

“But it’s really important that everybody is aware that there’s lots of broker flow out there that we like, there’s lots of brokers out there that we want to do more with, and we’re going to continue to push into that.”

Irvine concluded: “Continued growth in proprietary home lending is allowing us to adopt a more targeted approach in the broker market.”

“This, in combination with further delivery of seamless customer and broker experiences, is positioning us well to optimise growth and returns in this important market.”

According to NAB’s results for 1H26, the underlying profit created by the personal banking division increased by 3.7 per cent over the half.

Overall over 1H26, NAB’s Australian home lending balances rose 2.7 per cent, representing 1.1 times system (excluding the impact of the Advantedge run-off).

According to NAB’s 1H26 results, NAB wrote $48 billion in new Australian mortgages over the half, taking its Australian mortgage book to $373 billion (excluding Ubank), with $260.5 billion in personal banking ($173 billion of which is from proprietary lending), and $112.9 billion from the business and private banking division.

An additional $17.1 billion came from Ubank (up from 15.1 billion in 1H25).

As such, housing lending increased by $19.4 billion or 4.6 per cent since March 2025, mainly due to an increase of $11.8 billion (4.7 per cent) in personal banking, with growth of $17.3 billion or 7.8 per cent, driven by “continued growth in broker lending and improved growth in proprietary lending”.

Similarly, there was an increase of $6.9 billion or 6.5 per cent in home lending at the business and private banking division, also driven by improved growth in proprietary lending and continued growth in broker lending. Around 70 per cent of new sales for business lending are originated by proprietary channels.

[Related: NAB’s proprietary lending soars 46% in under 2 years]

Want to see more stories from trusted news sources?

Make The Adviser a preferred news source on Google.

Click here to add The Adviser as a preferred news source.