A tax debt whack could be on the way for small and medium-sized businesses. Finance brokers can play a key role advising SMEs on how to prepare and respond.

Help SME clients with upcoming tax pain

A tax-debt whack could be on the way for small and medium-sized businesses.

After 1 July 2025, taxpayers likely won’t be able to claim a tax deduction for the interest charged on money they owe to the ATO.

It would be a big change affecting many – about 65% of the outstanding $50 billion of ATO debt is owed by small businesses.

Finance brokers can play a key role advising SMEs on how to prepare and respond to the potential change.

“There’s a bit to be worried about here,” says Guy Callaghan, CEO of Banjo Loans.

“We’ve been tracking ATO debt for a while and it’s been increasing as a barrier for SMEs seeking finance.”

“Our SME Compass Report 2025 also found that 62% of businesses with an ATO debt saw the amount they owe increase last year. In addition, 77% of those businesses are on a payment plan and already paying interest to the ATO."

“Losing the ability to claim a tax deduction for this interest will put new pressure on thousands of SMEs,” Guy adds.

Understanding the proposed changes, and getting the right advice about how to act, will be critical.

What’s changing?

A lot of businesses owe the ATO money.

It could be that they haven’t paid tax on time because working capital is tied up with debtors, or perhaps due to large inventory balances.

Alternatively, it could be they submitted a tax return that wasn’t accurate, resulting in a shortfall that now needs to be paid.

In these two situations, the ATO charges interest on that money owed until it’s paid back – just like a bank.

Currently, businesses can claim a tax deduction for that interest.

But from 1 July 2025, if a proposed bill (Treasury Laws Amendment (Tax Incentives and Integrity) Bill 2024) passes, they won’t be able.

What does this mean for SMEs?

“With no tax relief on the interest charged, that ATO debt will effectively become more ‘expensive’,” says Callaghan.

“The tax burden becomes heavier.”

“Businesses will need to prioritise paying it back ahead of other costs – easier said than done when many smaller operators are already stretched,” he adds.

This new repayment-burden would be a new hit to business cashflow.

The proposed tax law change also suggests that the ATO will be zeroing in on outstanding debts.

How can brokers help?

SMEs with ATO debt will need to look at their cashflow cycle and build-in the outflows of tax debt repayments.

From this, they'll need to think about whether new finance – or a re-arrangement of their existing funding structure – will be needed to cover the tax debt.

Here, finance brokers can provide great advice and help to find a solution for business funding.

Adrian Palone, Business Advisory Partner at William Buck, outlines how brokers and advisers can further step-up and support SMEs.

“The first thing brokers can do is help clients to understand the impact of the proposed change on cashflow,” says Adrian.

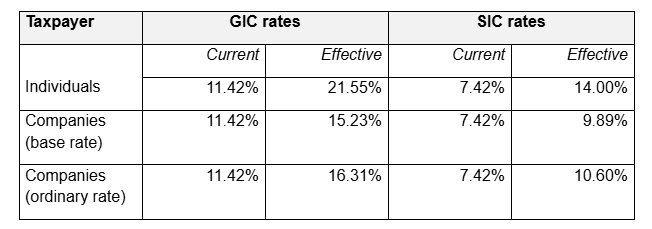

“Should this tax bill pass, and the existing tax deduction becomes unavailable, then the effective rates of interest payable increase dramatically – in some cases, nearly doubling.”

The below table shows what the change in interest rates would be on general interest charged (GIC) and shortfall interest charged (SIC) by the ATO.

“SMEs need to consider how they’re managing their existing tax obligations,” adds Adrian.

“Is it through their available cashflow, an ATO payment plan, or a debt facility – and is this strategy the best one available?”

Adrian suggests that if SMEs don’t know the answer, they can also speak with an accountant who’s qualified in working with the ATO.

“Accountants can liaise with the ATO and can often help taxpayers to have ATO interest amounts put on hold or even reversed.”

Businesses need to understand their options for reducing the risk of ATO interest charges. These include:

-

Talking to the ATO: engaging the tax office through a tax agent, putting in place a plan and understanding the nature of your tax debts can often see relief provided.

-

Getting it right first time: taxpayers need to work with their tax agents to ensure their tax returns are correct first time, every time. This way, the risk of a shortfall interest charge is reduced.

-

Managing cashflow: effective cashflow management systems allow business owners to clearly identify when a tax obligation may hit and empower them to plan accordingly.

-

Proactive tax planning: this will help SMEs better understand their tax obligations. If they don’t have a process to identify your options before 30 June each year, then they should talk to an accountant.

Flagging this potential, significant change with your clients, and that they should seek tax advice, is a great way to show your value as a key business adviser.

It’s also a timely opportunity to talk about the health of their cashflow and operations, and whether it’s time to explore a new funding arrangement.