According to industry veteran Nick Young of Trail Homes, while the year has been challenging, it’s not as dire as what was initially expected and there’s hope on the horizon.

Nick Young, the director of trail book lender Trail Homes, has outlined that while it’s easy to default to a ‘gloom and doom’ take-out for the year 2023, things are not as “dire” as they may seem.

Speaking to The Adviser, Mr Young explained: “It’s indisputably been a tough year for borrowers – particularly those who are exposed to high volumes of debt. That said, if we take cues from Australian Bureau of Statistics (ABS) data, it’s not as dire as what might be initially expected.

“The core reason for developing this piece is to put the current state of play into perspective by reviewing historical data and corresponding trends and overlaying this with where we are now. And, as the saying goes: ‘History has a habit of repeating itself.’ While the repeat may not necessarily be an ‘exact match’, retrospective data provides clear cues about what we can expect next.”

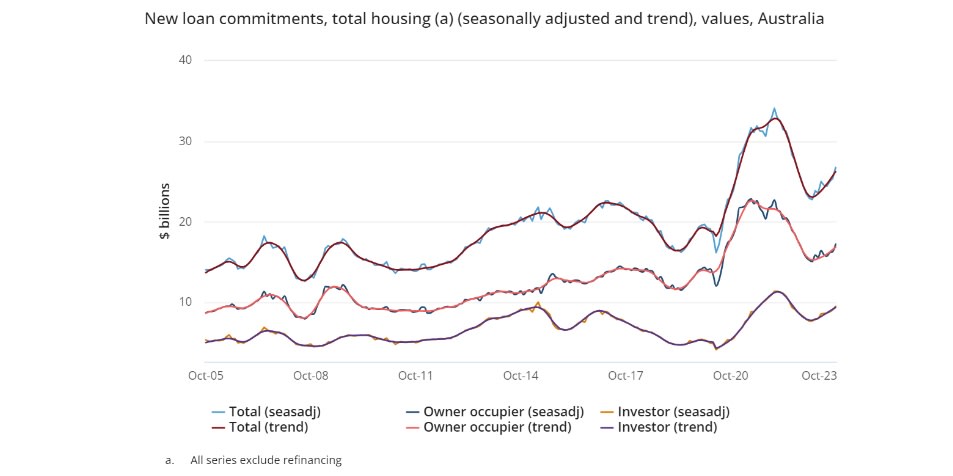

Mr Young flagged the following graph from the ABS as an example:

He flagged that while “things were tracking along nicely for quite some time”, when the global financial crisis (GFC) hit in 2007 and 2008, it created “the largest property bubble in history burst in the US, which then reverberated throughout Europe and Asia”.

“This fallout resulted in a sharp decline in economic activity, a rise in unemployment, and shattered consumer confidence globally,” he said, noting that there was a sharp decline in new commitments in Australia, followed by a period of dormancy, before a relatively equal ‘course correction’ in 2008.

“Australia, while affected, was largely cushioned compared to global markets.

“For those of us who experienced the GFC, it was a grim time, though relatively short-lived. Incidentally, along with this uptick came the boom of the non-bank sector, which flourished with market disruption.”

Mr Young drew parallels between the GFC and the COVID-19 pandemic – but added that the pre-and-post-COVID-19 trends are “unusual”.

“Similarly to pre-GFC, the economy was bullish before COVID-19 struck: then lending took off! There was a significant surge in loans spurred by excessive and ongoing government stimulus, marginal cash rates, and the message to SPEND to keep the country humming against the backdrop of a frightening scene globally,” he explained.

“But in extensive lockdowns, with consumer sentiment being struck hard – particularly in Victoria, spending was naturally down. Conversely, savings reached all-time records.

“There was only one way for this ‘artificial high’ to go: down. However, the question is whether the full extent has occurred yet.”

According to the Trail Homes director, he believes the initial indicators suggest that Australia has “dodged the bullet between the eyes”.

“We haven’t experienced the post-GFC low. In contrast, recently there’s been an uptick in new loan commitments both from owner-occupiers and investors, perpetuated by the seemingly never-ending refinancing,” he noted.

“This is in stark opposition to the initial fear that lending would proportionately inverse to the rise and get down to levels that we haven’t seen since 2011 – which would have been a recession. The surprise is in the hook: few picked that the economy would bounce and that it would coincide with the rest of the world.”

While Mr Young said that this “soft landing” is a welcome, unexpected turn, he warned “it should be treated with caution”.

“While rate increases are undoubtedly problematic, after historic lows, a recorrection is expected. The surprise is not that cash rates have risen, but more by the frequency, which, at least initially, didn’t correlate with consumer spending or sentiment. The market seems to be getting the memo to slow down spending, as acknowledged by the recent rate pause,” Mr Young said.

He continued that while there may be another rate hike in 2024, “hopefully we’re at or close to the end”.

Reflecting on the year that has been, Mr Young provided the following takeaways:

- What goes up must go down (how far is TBD).

- The ‘refinancing bonanza’ continues, albeit slowing.

- The RBA is prepared to be patient and the effect of inflation is substantial. “We encourage brokers to be on the front foot and put into place processes, systems, and/ or resources that support the proactive management of both personal and business borrowers (including debt consolidation and the consideration of alternative facilities, as appropriate). Ideally, this should be done in conjunction with the borrower’s accountant,” he said.

- Bond markets have seized up and it’s difficult to borrow money. “This is affecting not only rates, but also products and lenders’ credit profiles,” he said.

- Not all borrowers are in distress and opportunities are spurred by disruption. “This comment relates to both borrowers and lenders (hello, private lending),“ he said.

- Private lending is expected to continue to boom as the sector offsets the tightened credit appetite from traditional lenders (and, increasingly, non-bank lenders). The majors are expected to ‘stick to their lane’ and focus on vanilla residential mortgages, with commercial lending facilities and ‘non-prime’ borrowers directed to alternative lenders.

- Australia has a robust economy, though is not immune to geopolitical and global economic challenges.

Looking to the future, he told The Adviser: “With the concurrent rate rises, global geopolitical, and economic turbulence, combined with cost-of-living pressures, we’re on thin ice.

“The ice is holding at the moment, but we don’t know how strong the ice is. This is compounded by borrower’s ‘savings bubble’ that ballooned from the COVID-19 stimulus and unsustainable cash rates is now largely exhausted, leaving many borrowers uncomfortably exposed. The true effect of the increase in rates will be very raw in the absence of a cushion. That said, the level of delinquencies is holding better than what was expected.

“We expect 2024 to continue to be challenging, but hopefully not catastrophic and will favour those who are proactive, realistic, and open to different solutions.

“Brokers will remain at the helm to guide borrowers. We encourage the industry to take a well-deserved and very much-needed rest over the holiday period and focus on ‘taking the bull by the horns’ upon return in January.”

[Related: Business administrations surge, failure risk increases]

Want to see more stories from trusted news sources?

Make The Adviser a preferred news source on Google.

Click here to add The Adviser as a preferred news source.