When a client comes to you for finance on a unit or townhouse, the conversation tends to centre on the obvious numbers: the purchase price, the deposit, the rate and the repayment. The strata levy usually gets a passing mention as a line item in the serviceability calculation. The insurance sitting underneath that levy almost never comes up at all.

That is becoming a problem. Strata insurance has quietly moved from a back-office formality to one of the more volatile costs an apartment owner faces, and it now influences three things brokers care about directly: how much a client can borrow, whether a deal settles cleanly, and how much value you add as the person who saw the issue coming. Brokers who understand what is happening in the strata market are better placed to set client expectations, avoid late surprises at settlement, and have a more informed conversation than the agent across the table.

The headline number hides the real story

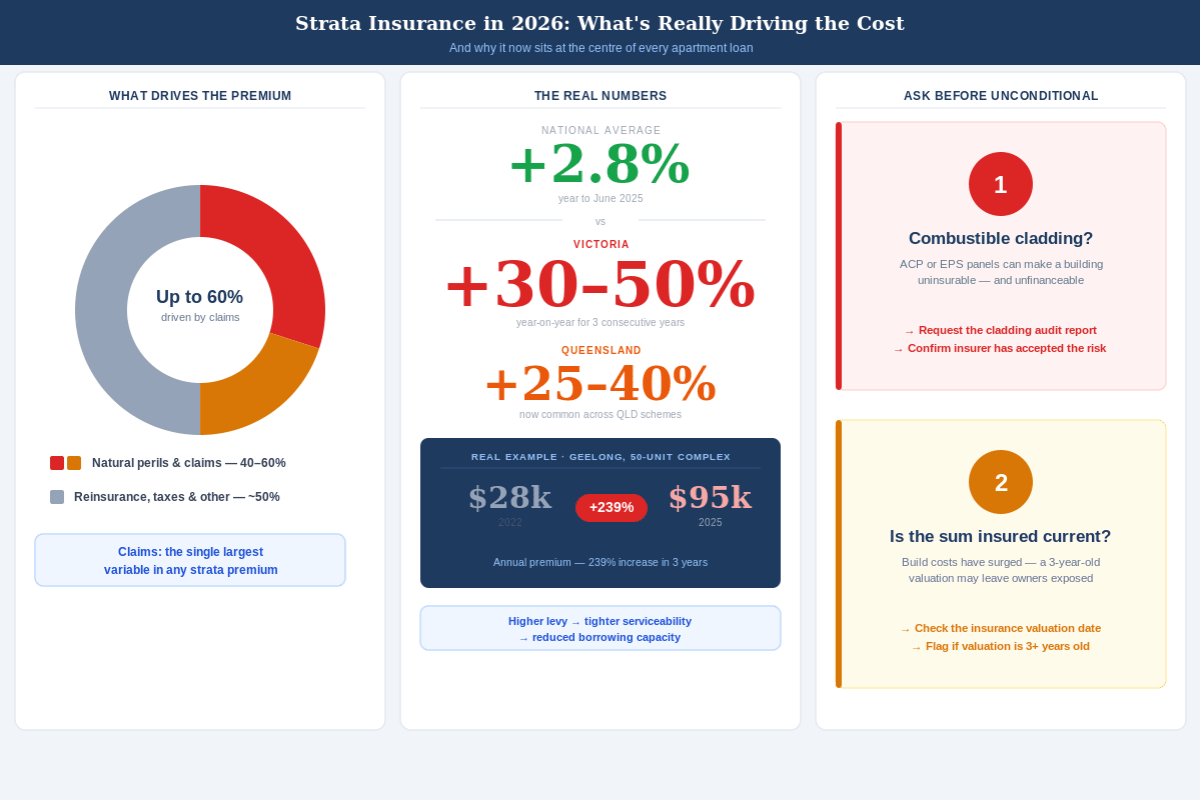

On paper, strata insurance looks stable. CHU's 2025 State of the Strata Market report put the average premium increase at 2.8 per cent in the year to June 2025, lifting the typical annual cost from $954 to $981 per lot. That is slower than wage growth and hardly cause for alarm.

The national average, though, flatters a lot of buildings. In Victoria, owners corporations have reported premium rises averaging 30 to 50 per cent year-on-year for three years running. In Queensland, increases of 25 to 40 per cent have become common. The worst cases are eye-watering: one 50-unit complex in Geelong saw its premium climb from $28,000 in 2022 to $95,000 in 2025, a 239 per cent jump in three years.

That cost does not disappear into thin air. It flows straight into the quarterly strata levy, and the strata levy flows straight into your client's serviceability assessment. A client who comfortably qualified on last year's levy figure can look very different once a building's insurance renews 40 per cent higher. For buyers stretching to get into a complex in a cyclone-exposed or flood-prone postcode, the insurance line can be the difference between an approval and a decline, and it is the one number nobody thinks to check until late in the piece.

(Graphic: Strata insurance numbers. Credit: Custom)

everyday "attritional" claims such as water damage and minor property damage. The first half of 2025 alone brought Tropical Cyclone Zelia, ex-Tropical Cyclone Alfred and widespread flooding across several states, all of which feed into how insurers price the buildings in those regions.

Newer risks are starting to bite too. Lithium-ion battery fires, from e-bikes and scooters stored in apartments and car parks, are an emerging concern for insurers, with fire services recording a sharp rise in incidents through 2025. None of this means a client should avoid apartments. It means the building's location, age, claims history and risk profile matter more than they used to, and those factors vary enormously from one complex to the next.

The settlement risk most brokers never see coming

Premium size affects borrowing capacity. Insurance availability affects whether the loan settles at all, and this is where the real exposure sits.

Adequate building insurance covering the strata scheme is a standard condition of virtually every mortgage. The lender is securing its money against the building, so it needs that building properly insured for its full reinstatement value. When a strata scheme cannot get adequate cover, or is badly under-insured, the deal has a problem that no amount of rate-shopping will fix.

Two issues are driving this. The first is under-insurance. With construction costs having surged, a sum insured set a few years ago can fall well short of what it would now cost to rebuild, especially in buildings with known defects where the real repair bill is higher than a standard valuation assumes. If a major loss occurs and the payout falls short, owners are personally on the hook for the gap.

The second is defects and combustible cladding. Buildings carrying non-compliant aluminium composite panels or expanded polystyrene have, in some cases, become difficult or impossible to insure, and the cost to rectify can run into the tens of thousands per unit. An apartment in an affected building can be rendered effectively unsaleable and uninsurable, which means it is also effectively unfinanceable. A broker who knows to ask about the building's insurance status, cladding and defect history before the contract is unconditional can save a client from a deal that was never going to settle, and save themselves a clawback.

A practical habit worth building: when a client is buying into a strata scheme, encourage them to obtain the strata records, including the certificate of currency, the insurance valuation date and any reference to cladding or defects, as part of their due diligence. It sits naturally alongside the strata report most buyers already commission, and it surfaces the insurance question while there is still time to act on it.

Where this leaves you in 2026

The outlook offers some relief. The market softened through the latter part of 2025 and that competitive tone is expected to continue into 2026, which should mean more options and steadier pricing for many schemes. A September 2025 review by the Australian Reinsurance Pool Corporation also confirmed that strata premiums under the cyclone pool would remain unchanged, with pricing judged adequate for the risk.

Softer conditions, though, only help schemes that actually shop the market and hold an accurate, current building valuation. Plenty do neither. They auto-renew, carry a sum insured that no longer reflects rebuild costs, and never test whether a better-priced or better-structured policy is available. That gap between what a building pays and what it could pay is exactly where good advice earns its keep.

You are not expected to become a strata insurance expert, and you shouldn't try to be. But knowing enough to ask the right questions, and knowing who to point a client to when the answers raise a flag, is squarely part of looking after them. When a client's building is facing a steep renewal, is under-insured, or is wrestling with a defect or cladding issue, the most useful thing you can do is connect them with a specialist who works in that market every day. A conversation with a broker who specialises in strata insurance can identify whether a scheme is over-paying, properly valued, and appropriately covered, often well before a renewal notice or a finance condition forces the issue.

Strata insurance is not going to become less relevant to apartment lending. The brokers who treat it as part of the picture, rather than someone else's problem, will write cleaner deals and keep clients who remember who flagged the issue first.

Want to see more stories from trusted news sources?

Make The Adviser a preferred news source on Google.

Click here to add The Adviser as a preferred news source.